90% of homeowners underestimate the costs of owning a home1, and 73% have regrets about their home purchase. To sidestep such underestimation and regret, let’s consider all the costs of owning a home, how to estimate them, and how to lower them.

Note that this article is about the costs of homeownership rather than the upfront cash needed to buy a home in the first place. If you’re interested in the latter, feel free to check out this other article we wrote about that.

Average Costs of Owning a Home

Below are the average costs of homeownership in the United States. They add up to a whopping $3,598.58 per month. Each will be covered in more detail, both in terms of how to estimate it and how to lower it. If you’d like to skip ahead to any of them, feel free to click its link.

- Mortgage Costs: $2359.28/month

- Capital Expenses: $367.99/month

- Maintenance: $242.47/month

- Utilities: $269.58/month

- Property Taxes: $2,795/year

- Home Insurance: $1516/year

- Average Monthly Total: $3,598.58

There are two additional costs that may or may not apply to you. These were not included in the cost total but we will still cover them:

Mortgage Costs

Let’s start with the big one, mortgage costs. These are basically determined by three factors:

- Mortgage Amount

- Loan term

- Interest rate

Mortgage Amount

The mortgage amount is the dollar amount the bank lends you for buying a home. Basically, it’s the property’s purchase price minus the amount of money that you pay upfront as a down payment. A higher mortgage amount means higher monthly payments. We calculate that the average mortgage amount for new homebuyers is about $299,388, given an average property price of $348,1262 and an average down payment of 14%3.

Loan Term

The loan term is the span of time that the bank gives you to repay a loan. A longer loan term means lower monthly payments. By far the most common loan term is 30 years, which is typically the longest available.

Interest Rate

An interest rate is basically the percent of your loan amount that is added to said loan amount annually. You can shop around for lower rates, but usually they will all be similar for the kind of loan you want. At the time of writing they’re sitting at 7.58% for 30 year fixed-rate mortgages, but they fluctuate often. Feel free to check out this handy tool from Bankrate to see where they’re at now.

Homebuyer Tips for Lower Mortgage Costs

- Maximize your loan term, typically 30 years.

- Settle for a less expensive property.

- Save money to increase your down payment.

- Lower your interest rate by increasing your credit score or by shopping around for lenders.

Homeowner Tips for Lower Mortgage Costs

- Refinance for a lower interest rate or to extend or reset your loan term.

- If you’re struggling to make payments, banks will sometimes even let you modify your loan to have a 40-year loan term.

Capital Expenses

Capital expenses, or CapEx, are the large and expensive components of a house—things like the roof, furnace, cabinets, and so on. As a function of the impermanence of everything, all those items will eventually deteriorate and need to be replaced. And they aren’t cheap.

According to HomeAdvisor, the average cost to replace a roof in the U.S. is $9,154. Combine that with the fact that the most common type of roof (asphalt shingles) tends to last around 20 years, and we conclude that the average U.S. property owner should budget around $457 every year, or around $38 per month, to cover the eventual replacement of their roof.

That’s just one capital expense—there are about 18 other common ones. Below is a full list as displayed in the HomeEstimator app, alongside the average U.S. replacement cost and lifespan for each4.

Homebuyer Tips for Lowering Capital Expenses

- Settle for properties that have fewer capital expenses, such as those lacking a garage, a wooden retaining wall, or central AC.

- Before buying a property, have it inspected. If the inspection shows that any of the capital expenses are ready to be replaced, negotiate with the seller accordingly. Sometimes sellers will lower the purchase price or have capital expenses replaced before sale.

Homeowner Tips for Lowering Capital Expenses

- The price to replace a capital expense can vary dramatically across contractors and agencies (I was once quoted $20,000 for a roof replacement for which I ended up paying another contractor $8,500). When it’s time to replace a capital expense, call around and get multiple quotes.

- Often you will be charged less by independent and smaller-scale contractors, as they have lower overhead expenses. A good place to find recommendations for contractors like that is on the website Nextdoor.

- For some capital expenses, you can get a better deal based on the time of year. For example, you’ll generally pay more if you have your furnace replaced in the middle of winter as compared to the spring or fall.

Maintenance

In contrast with capital expenses, which are fairly specific and predictable, maintenance covers the unpredictable: busted toilets, leaky pipes, flickering lights, even pest control. To account for these and other things, we reach for time-tested methods often used by real estate investors.

First is the 1% Rule. This just assumes that maintenance will cost about 1% of a property’s value per year. For a $300,000 property, that would be around $3,000 per year, or $250 per month. The reasoning is that expensive properties tend to have expensive components or tend to be located in areas with more expensive prices.

Second is the Square Footage Rule. This basically assumes that maintenance will cost about $1 per square foot per year. The idea here is that the more square feet there are, the more opportunity there is for things to go wrong. 2,400 square feet means $2,400 per year which divides to $200 per month.

Finally, there’s the hybrid method5, which is just an average of the first two. So if the 1% Rule yields $250 per month, and the Square Footage Rule yields $200 per month, we’d go with the number right in between: $225 per month.

Homebuyer Tips for Lowering Maintenance Costs

- Buy a smaller property.

- Buy a less expensive property with simpler components (do you really need an AI laundry machine?).

- Buy a newer property.

Homeowner Tips for Lowering Maintenance Costs

- Learn to DIY.

- As with replacing capital expenses, compare quotes from multiple maintenance providers and check Nextdoor for local recommendations.

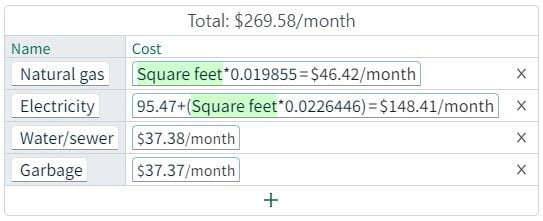

Utilities

Generally, there are four types of utilities to think about when calculating home costs:

- Water & sewer

- Garbage

- Electricity

- Natural gas

For the most accuracy you’ll want to estimate each utility separately and add them up.

If you already pay for some utilities, you could start by estimating based on what you currently pay. If you aren’t used to paying for utilities, ask around or look up the prices in your area. Depending on how fancy you want to get, you could also factor in property square footage for calculating the utilities used for heating and cooling: fewer square feet means less space to heat and cool, which means lower energy bills.

In 2021, Homeowners spent on average around $3,235 per year on the above utilities6, or about $270 per month. Below you can see an itemized version of the national average that takes square feet into account for utilities commonly used for heating and cooling.

Homebuyer Tips for Lowering Utility Costs

- Buy a property that has fewer square feet. On average, heating and cooling account for roughly half of a household’s energy usage7, so fewer square can lead to significantly less energy usage.

Homeowner Tips for Lowering Utility Costs

- Take energy saving measures such as using all LED lights, weatherizing windows, and adding insulation.

- Dress appropriately so you can be more comfortable with less heating and cooling.

Property Taxes

According to the Real Estate Witch survey referenced at the top of the article, property taxes are the most underestimated cost of owning a home. That’s understandable, as property taxes are prone to unpredictable change, as they are influenced by such unpredictable things as home price fluctuations and the budgetary constraints of local government. In any case, we’ll do our best.

Usually you can find a property’s taxes for the current year listed right on the MLS. Otherwise, you should be able to look up official property tax records online, like through your county’s website. Beware that some states have laws in place that could result in significant tax increases upon the purchase of a home. Michigan, for example, prohibits tax increases higher than 5% per year except for when a property is purchased, at which time its taxes may catch up to what they would have been without the 5% limit. That is to say, you may want to do a bit of research to see if there are any laws like that in your area.

Finally, consider that property taxes generally increase over time. Fortunately, that often happens in tandem with increases in property value. Unfortunately, that doesn’t necessarily help your monthly budget, at least not in the short-term.

Home Insurance

The average homeowner pays $1516 per year for home insurance, or about $126.33 per month. But prices vary greatly depending on area and type of home. For instance, a $225,000 duplex in Saint Paul, MN costs over $2,600 per year to insure—over $1000 more than the national average.

To size up insurance for the type of property you’re interested in, first you need an insurance agent or broker. If you don’t have one, pick a property on the MLS and use it to test agents and brokers for quotes. Once you have an insurance person, ask them for quotes on a couple properties that approximate the type of place you’re looking for. Pretty quickly you should start to get a sense of the cost of insurance for the kind of property you want.

To get fancy, you might take a close look at a few quotes you get and use them to dial in an equation for estimating insurance costs that adjusts based on factors like square feet or unit count (in the case of multi-family properties).

The above is great for estimating insurance costs for large numbers of properties in the early stages of the buying process. That said, if you intend to make an offer, we recommend first having your insurance person verify the cost to insure the property so that there are no surprises.

Optional-ish Costs of Owning a Home

There are a couple other costs that may or may not be relevant to you. It all depends on what kind of property you’re looking for and how much work you’re willing to do (or how much work your kids are willing to do).

Yardwork

Lawn mowing, leaf raking, snow shoveling, gutter cleaning—unless you’re buying a condo, you will need to handle these tasks one way or another. And if you won’t do them yourself—not to mention your other household members or HOA—then there will be sizable a cost. According to Statista, the average family paid $503 per year on yardwork in 2017, and with inflation and everything, the cost has almost certainly increased significantly since then.

HOA Fees

Finally, we have arrived at HOA fees: money paid to Homeowners Associations. Unlike yardwork, you’re actually much more likely to run into these if you buy a condo—though townhomes and houses can also be subject to them. In exchange for HOA fees, HOAs often provide various things: maintenance, yardwork, neighborhood rule enforcement, etc. They can differ greatly between one another, though, so use due diligence before buying a property that’s associated with one. The average homeowner who pays HOA fees shells out around $250 per month according to iProperty Management.

Closing Thoughts on Costs of Owning a Home

Note that most of the covered costs will generally increase over time, whether due to inflation or to increases in property value. That is to say, if the costs of a home fit your budget right now, they might not always if your income doesn’t keep pace.

There you have it, a complete rundown of the costs of owning a home, how to estimate them, and some tips for homebuying with an eye for lowering them. If you want some help with adding up home costs for yourself, we again invite you to check out our HomeEstimator app, which can factor in all of the costs discussed in this article.

- Home cost underestimation and homebuyer regret statistics according to Real Estate Witch ↩︎

- Average property purchase price according to Zillow ↩︎

- Average down payment percent according to the National Association of Realtors ↩︎

- Average CapEx replacement costs are from HomeAdvisor, and average CapEx lifespans are from the National Association of Homebuilders (NAHB) ↩︎

- The hybrid maintenance calculation method is what we used to calculate maintenance costs at the top of the article, given the average property price according to Zillow and average square footage of 2,338 according to the NAHB ↩︎

- The utility total is according to a report from the Bureau of Labor Statistics (BLS) ↩︎

- Heating and cooling estimates are from the U.S. Energy Information Administration ↩︎